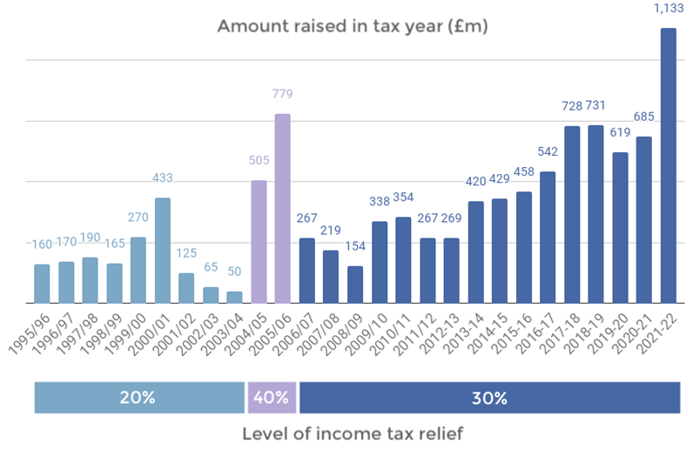

VCT fundraising has reached a new high in 2021-2022, even more than in 2005 when the max level of income tax relief was capped at 40% (against the 30% in place since 2006).

And yet, companies that have been founded by VCTs in the past have a hard time getting a follow-on investment from their lenders.

VCTs, or Venture Capital Trusts, are a type of investment fund that provides venture capital to small, unquoted companies. VCTs were introduced by the UK government in 1995 to encourage investment in small businesses and to help them grow.

Partner at Maven, Ewan MacKinnon shared: “VCTs are playing an ever-more important role in supporting the growth and success of ambitious young businesses, helping to stimulate both innovation and the creation of skilled employment across a range of exciting sectors."

More funds are opening for subscriptions every year. Nick Britton, head of intermediary communications at the Association of Investment Companies, shared: “There’s strong demand for VCTs from investors, with a record £1.13bn raised last tax year.”

“Some of this is the result of the squeeze on the pension annual allowance for high earners, which has encouraged the likes of doctors and dentists to look at tax-efficient investments.”

VCTs are a win for everyone involved: Investors (LPs), targeted companies, and the funds themselves. Everyone’s a winner. But that comes with conditions.

Some of these conditions are why companies funded by VCTs have a hard time getting a follow-up investment.

With that in mind, let’s review what VCTs are about, and discuss a recent development in how VCTs manage their funding portfolio.

Important Facts about VCTs

Here are some key things to know about VCTs:

- Tax benefits: One of the main reasons investors choose VCTs is the tax benefits they offer. Investors can receive a 30% income tax relief on investments of up to £200,000 per tax year. In addition, any dividends received from the VCT are tax-free, and any gains made on the sale of VCT shares are exempt from capital gains tax.

- High-risk, high-reward: VCTs invest in small, unquoted companies, which are considered higher-risk than larger, publicly traded companies. However, they also offer the potential for higher returns if the companies they invest in are successful. They are usually able to hedge against failed companies and provide steady returns, nonetheless.

- Limited liquidity: VCTs are typically listed on a stock exchange, but they can be illiquid investments, meaning it can be difficult to sell shares if there isn't a buyer available.

- Investment minimums: VCTs often have high minimum investment requirements, which can make them inaccessible for some investors. On the flip side, they are more accessible to investors than VC.

Manager expertise

VCTs are managed by professional fund managers who have experience in identifying and investing in high-growth potential companies. These VCTs managers, in turn, expect CEOs and CFOs of the companies they backed the following: They want the management team of that company to have the willingness and the capability to scale up.

That means VCTs expect the managerial team of the backed company to be knowledgeable about scaling a company. Either by being repeating entrepreneurs, who have done this before; or have hired (or are willing to hire) competent staff who has prior experience doing so.

The success of the VCT fund is predicated on that scaleup, so this condition is understandable. In the same vein, managers are expected to keep an open mind about their VCT partners’ pieces of advice regarding scaling up.

Investment Restrictions & Health Check

VCTs must follow certain investment restrictions set out by the government, including limits on the size and age of the companies they can invest in. All companies must keep rigorous “eligibility” standards.

This is regulated by “health checks” which have become a cornerstone of VCT’s regulatory legislations. These controls were designed so that VCTs, to an extent are not funding “zombie” businesses. The legislation existed prior, but since 2018, the HMRC started tightening the screws on it.

This legislation is paramount to make stakeholders’ investments more secure by preventing misuse of the VCT tax relief scheme and ensuring that VCTs invest in eligible companies.

The health check evaluates whether the portfolio company meets the eligibility criteria, such as qualifying company status, investment requirements, and non-qualifying company status.

Financial health is also a prominent factor. Organic revenue is under the microscope here, as well as the companies’ debt balance. If the health check determines that the company no longer meets the eligibility criteria, the VCT is prohibited from making further investments.

Instances have occurred where companies failed to receive follow-on investments from VCTs due to the health check. For example, in 2019, Circassia, a UK-based pharmaceutical firm, was unable to secure additional investment from VCTs because it breached the VCT investment requirements, despite having received over £200 million from VCTs in the past.

Imagination Technologies, a technology firm, also experienced a similar situation, where VCTs did not provide follow-on investment after the health check revealed the company no longer met the eligibility criteria. Octopus Ventures, a major VCT provider, had previously invested £15 million in Imagination Technologies.

In Conclusion

VCT are outstanding funding partners, but the criteria that enable them to keep investing in a company are quite strict, as it can, and do penalise some of their partners.

Whether it is about keeping your company in check of these criteria or finding a debt facility which allows for more wiggle room, you can always find a solution to get the most out of your VCT partnership.

Talk to one of our advisors to get a clear view of your options.

.png)